Who can hold security for expenses under the Party Wall etc. Act 1996?

This paper explores and clarifies why holding security for expenses is a regulated activity under financial services legislation, what exceptions there may be, and which supervisory authority might be appropriate in the context of the PWA.

16 July 2026 | by Mikael Rust

First published in the peer reviewed Journal of Building Survey, Appraisal & Valuation

Vol. 15. No. 1, 2026

© Henry Stewart Publications

Download a pdf of the journal article

Following a number of cases in the High Court, the Solicitors Regulatory Authority[1] (SRA) issued a warning in December 2014 against the improper use of solicitors’ client accounts as a banking facility. As a result, solicitors were no longer happy to hold security for expenses under the Party Wall etc. Act 1996 (PWA) unless they were also giving legal advice as a solicitor in connection with the PWA.

There being no readily accessible alternative, this created a practical problem for building owners required to give security, and a number of companies began offering to do so as ‘escrow agents’ or stakeholders. Some, but not all, are regulated and supervised under the Payment Services Regulations 2017 (PSR 2017) and there is confusion among surveyors and the unfortunate parties caught up in the PWA process as to what legal requirements must be met before someone can provide what appears to be a simple and obvious service.

The complication arises from the fact that the very act of holding security for expenses involves a person or entity accepting money from one party with the sole and specific intention that it may be paid to one or more third parties. Anyone offering such a service is providing a payment service as defined in PSR 2017 and must be regulated by a designated supervisory authority.

This paper explores and clarifies why holding security for expenses is a regulated activity under financial services legislation, what exceptions there may be, and which supervisory authority might be appropriate in the context of the PWA.

SECURITY FOR EXPENSES

Section 12 of the Party Wall etc. Act 1996 (PWA) provides that if either party requires security for expenses, the other party shall ‘give such security as may be agreed between the owners or in the event of dispute determined in accordance with section 10’. While there is no stipulation as to what form such security should take, if, as is usually the case, the matter of security is referred to the surveyors as a ‘dispute’, the preferred form of security is for an agreed sum to be placed with a stakeholder in what is commonly referred to as an escrow[2] account. Other options may be agreed, but this is usually the simplest, enabling the parties and their surveyors to retain some control over the security provided.

The accepted arrangement is, in simple terms, for a stakeholder to receive a sum of money (the security sum) from the person giving security (PGS) and hold the money until directed to return it or to pay some or all of it to the other party and/or to another third party. This is not escrow in the strict legal sense, but the term is in general use in the context of the PWA and similarly referenced in Financial Conduct Authority (FCA) guidance[3] and the Solicitors Regulatory Authority (SRA) warning issued in December 2014 against the improper use of solicitors’ client accounts as a banking facility.

For convenience, this arrangement is referred to in this paper as ‘holding security under the PWA’.

THE REGULATIONS

Financial services in the UK are subject to the Financial Services and Markets Act 2000 (FSMA), as amended by the Financial Services Act 2012 (FSA 2012), which implemented the current regulatory framework for financial services in the UK. It replaced the existing Financial Services Authority with two new regulators, the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA). The Electronic Money Regulations 2011 (EMR 2011),[4] The Payment Services Regulations 2017 (PSR 2017) and the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (AMLR 2017) are the regulations made by the Secretary of State under FSMA 2000 as amended by FSA 2012 currently governing financial activity in the UK.

The sequence of legislation, regulations and orders and when they came into force can be helpful in understanding their cumulative effect:

- Financial Services and Markets Act 2000 (1st December, 2001).

- The Financial Services and Markets Act 2000 (Regulated Activities) Order 2001.

- The Financial Services and Markets Act 2000 (Professions) (Non-Exempt Activities) Order 2001.

- The Money Laundering Regulations 2007.

- The Payment Services Regulations 2009 (2nd March and 1st May, 2009).

- The Financial Services and Markets Act 2000 (Regulated Activities) (Amendment) Order 2009 (1st July, 2009).

- The Electronic Money Regulations 2011.

- Financial Services Act 2012.

- The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (26th June, 2017).

- The Payment Services Regulations 2017 (13th August, 2017).

- The Payment Services (Amendment) Regulations 2024.

This paper addresses whether holding security under the PWA constitutes financial activity under those regulations and the resulting implications. For reasons that hopefully will become clear, we will be jumping down and up this list as the picture unfolds.

PSR 2017

PSR 2017 are the regulations currently governing payment services in the UK which, as we will discover below, does include holding security under the PWA as well as other escrow services.

Available guidance

The FCA Handbook[5] offers guidance and sets out the rules as they are applied by the FCA. The Handbook covers all activities regulated by the FCA and the print version runs to 23 loose-leaf volumes of rules and standards, reflecting the complexity and breadth of the regulations. Fortunately, not all the content is relevant to payment services. The section that most directly applies is the Perimeter Guidance Manual (PERG)[6] in the Regulatory/Registry Guides section, specifically PERG 15 – Guidance on the Scope of the Payment Services Regulations 2017.[7]

The FCA publishes another, rather more helpful, document, ‘Payment Services and Electronic Money – Our Approach’[8] (FCA Approach Document), with the stated aim of helping businesses to understand the FCA’s general approach and to navigate PSR 2017 and the FCA’s rules and guidance. This is the document to which the FCA will refer applicants making use of its pre-application support service[9] (PASS). Nevertheless, the FCA recognises that ‘The interpretation of financial services legislation is ultimately a matter for the courts. How the scope of the PSR 2017 affects the regulatory position of any particular person will depend on his [sic] individual circumstances.’[10]

Is holding security for expenses a payment service?

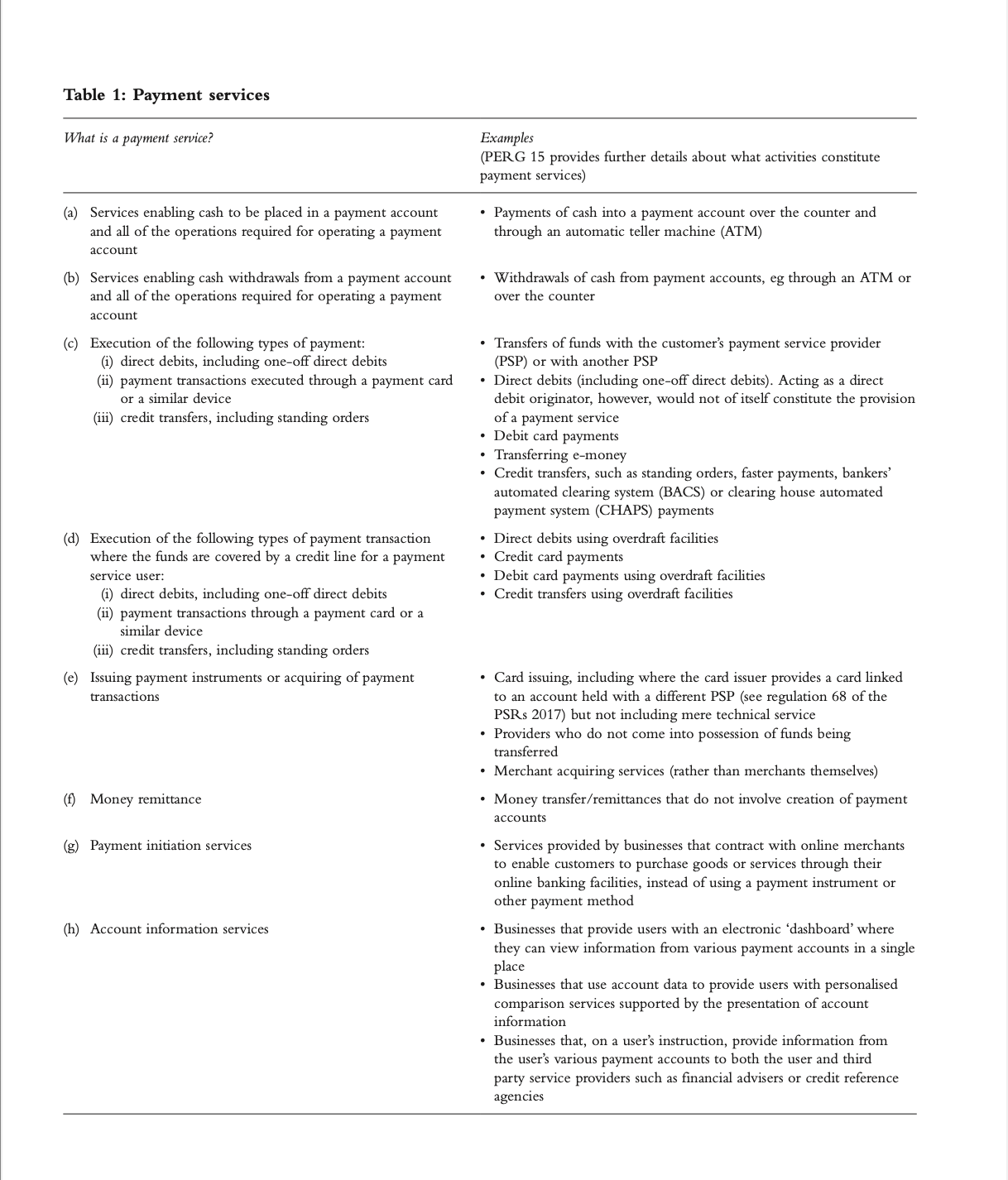

Eight payment services are defined in PSR 2017. These are listed in Schedule 1 Part 1 and are themselves subject to the many definitions in regulation 1. EMR 2011 refers to PSR 2009 in defining payment services but the FCA Approach Document clarifies its own understanding and application of these definitions for both PSR and EMR, reproduced here in Table 1.

Although the document caveats that ‘PERG 15 provides further details about what activities constitute payment services’, it is clear that holding security for expenses under the PWA does — and in the vast majority of cases could only — come under (f) money remittance: ‘money transfer/ remittances that do not involve creation of payment accounts’.

Regulation 2 of PSR 2017 defines ‘payment account’ as ‘an account held in the name of one or more payment service users which is used for the execution of payment transactions’, which would be an unusual and unnecessarily onerous facility for the holding of security under the PWA. For the purpose of this review, the only material difference between EMR 2011 and PSR 2017 is the way in which security might be held and access to it by the parties and surveyors. This is a significant distinction for the parties and surveyors themselves to consider very carefully. Regulation 2 of EMR 2011 defines electronic money (e-money) as:

electronically (including magnetically) stored monetary value as represented by a claim on the electronic money issuer which —

(a) is issued on receipt of funds for the purpose of making payment transactions;

(b) is accepted by a person other than the electronic money issuer; and

(c) is not excluded by regulation 3.

The exclusions in regulation 3 are not relevant to holding security, and e-money as defined here is not a form of security that would be acceptable to most party wall surveyors simply because it must be ‘issued on receipt of funds’. In other words, it is not held in escrow by the stakeholder.

In clarifying how e-money is defined, paragraph 2.35 of the FCA Approach Document suggests ‘Examples of e-money include prepaid cards that can be used to pay for goods at a range of retailers, or virtual purses that can be used to pay for goods or services online’.

Guidance from PASS is that the only permission required for holding security for expenses under the PWA is money remittance. Further permissions such as ‘faster payments, BACS or CHAPS payments’ referred to under service (c) are not required.[11]

Holding security for expenses is, therefore, money remittance, a payment service under the regulations, and anyone offering that service is a PSP under PSR 2017.

With very few exceptions, PSPs must register with the FCA as a small payment institution[12] (SPI) or an authorised payment institution[13] (API), and are required to make standard regulatory returns under the FCA’s RegData reporting schedule, while being supervised by FCA or HM Revenue & Customs (HMRC) for Anti-Money Laundering. There would be no need or purpose to register as an Electronic Money Institution (EMI) unless the stakeholder intends to issue e-money for the purpose of making payment transactions.

THE MONEY LAUNDERING, TERRORIST FINANCING AND TRANSFER OF FUNDS (INFORMATION ON THE PAYER) REGULATIONS 2017 (AMLR 2017)

Under regulation 27, ‘A relevant person must apply customer due diligence measures if the person establishes a business relationship …’

Under regulation 8(2)(b), a ‘relevant person’ includes ‘financial institutions’.

Under regulations 3(1) and 10(2)(a), a ‘financial institution’ means ‘an undertaking, including a money service business, other than an institution referred to in paragraph (3), when the undertaking carries out one or more listed activity’.

Under point 4 of Schedule 2, ‘Listed Activities’ include ‘Payment services as defined in regulation 2(1) of PSR 2017’.

Given that holding security for expenses is undertaking payment services, anyone doing so is a relevant person for the purposes of AMLR 2017.

‘Business relationship’ is defined in regulation 4(1) as:

a business, professional or commercial relationship between a relevant person and a customer, which—

(a) arises out of the business of the relevant person, and

(b) is expected by the relevant person, at the time when contact is established, to have an element of duration.

It should be noted that the position of HMRC is that entering into an agreement with and accepting funds from the PGS is to enter into a business relationship for the purpose of the regulations, even if, as is usually the case, the security sum is eventually returned in full to the PGS with no third party payment (money remittance) being made. The explanation offered for this by HMRC is that simply by accepting funds from a client into your bank account and then returning them you could, inadvertently, be money laundering. Know your customer (KYC) due diligence must be undertaken before funds can even be accepted.

Clearly it would not be consistent with the powers conferred by the PWA on surveyors appointed and selected under it for one of those surveyors to enter into a business relationship with any of the parties. The only exception might be where the building owner’s surveyor adds the holding of security to a business relationship established with the building owner before any notice was served.[14]

Exceptions

Occasional or very limited basis

AMLR 2017 regulation 15(2) provides an exclusion from the requirement for registration where the financial activity is provided on an ‘occasional or very limited basis’ as defined in 15(3). In order to qualify, all seven conditions must be met including, crucially, ‘(e) the financial activity is not the transmission or remittance of money (or any representation of monetary value) by any means’. This means that anyone engaged in ‘money remittance’ cannot claim exemption from registration on the basis of ‘occasional or very limited basis’ even if the other six conditions are satisfied.

Given the purpose of the regulations is to combat financial crime, it does seem unlikely that the regulators would be inclined to leave a ‘no questions asked’ loophole in a regulated environment where substantial sums may be transferred, if only on ‘an occasional or very limited basis’.

Ancillary to another business activity

FCA guidance in PERG 15.2 takes the form of Q&As in which Q9 asks: ‘If we provide payment services to our clients, will we always require authorisation or registration under the regulations?’

Simply because you provide payment services as part of your business does not mean that you require authorisation or registration. You have to be providing payment services, themselves, as a regular occupation or business to fall within the scope of the regulations … In our view this means that the services must be provided as a regular occupation or business activity in their own right and not merely as ancillary to another business activity …

The fact that a service is provided as part of a package with other services does not, however, necessarily make it ancillary to those services – the question is whether that service is, on the facts, itself carried on as a regular occupation or business activity.

In its answer to Q33A, PERG 15.2 addresses escrow services directly:

An example of an e-commerce platform that is likely to need to be authorised or registered by the FCA is one that provides escrow services as a regular occupation or business activity. Escrow services generally involve a payment service consisting of the transfer of funds from a payer to a payee, with the platform holding the funds pending the payee’s fulfilment of certain conditions or confirmation by the payer. It should be kept in mind that an escrow service may be a regular occupation or business activity of a platform even if it is provided as part of a package with other services.

Some practitioners argue that where holding security is intrinsically linked to another activity, such as appointment or selection under section 10 of the PWA as one of the surveyors for that particular project, then the service may be regarded as ancillary to that primary activity, and the provider would not require authorisation or registration under the regulations. The fact remains, however, that the service is still money remittance, which is precluded from exemption by virtue of regulation 15(3)(e).

SUPERVISORY AUTHORITIES

PSPs must be supervised for anti-money laundering by supervisory authorities. AMLR 2017 regulation 7 lists the bodies designated as supervisory authorities. For most money service businesses (MSB), which includes PSPs, the supervisory authority is the FCA. Regulation 7(1)(c) provides that MSBs not supervised by the FCA are supervised by HMRC. Whether an MSB is supervised by FCA or HMRC or both depends on which payment services it provides. If the only service provided is money remittance, HMRC is the supervisory authority. For all other payment services FCA is the supervisory authority. FCA and HMRC may agree between them which shall be the supervisory authority for an MSB falling under both.

Schedule 1 lists 22 ‘self-regulatory organisations’ all, except the Faculty Office of the Archbishop of Canterbury, being legal or accountancy organisations. Regulation 7(1)(b) states that ‘each of the professional bodies listed in Schedule 1 is the supervisory authority for relevant persons who are members of it, or regulated or supervised by it’. Significantly in the current context, the Royal Institution of Chartered Surveyors (RICS) is not included, and neither is any property or construction-related organisation.

Exempt Professional Firms (EPF)

Part XX of FSMA 2000 provides for the ‘Provision of Financial Services by Members of the Professions’ enabling HM Treasury to designate professional bodies (DPB) to ‘supervise and regulate the carrying on of exempt regulated activities by members of the professions in relation to which they are established’.

There are only 15 DPB Regulated Activities, all described at length, in The Financial Services and Markets Act 2000 (Regulated Activities) Order 2001[15] (Regulated Activities Order). Most are related to investment advice but two might be seen to have relevance to holding security for expenses.

The first is ‘Accepting Deposits’ (Chapter II). Article 5 of the order describes in detail both what constitutes a deposit and what exclusions apply. It is clear that holding security for expenses under the PWA is not ‘Accepting Deposits’.

The second is the issuing of e-money which appears in both the Regulated Activities Order and PSR 2017. This is defined in EMR 2011 and included in (c) (ii) in the Payment Services table (see above). Some practitioners understand this to mean that RICS can license its members to issue e-money and so it might until EMR 2011 came into force making clear in its guidance notes:[16] ‘Parts 2 to 4 of these regulations establish a new authorisation regime for electronic money issuers.’

RICS did become a DPB in 2006, but, as stated on its own website, its DPB scheme is approved by HM Treasury solely to regulate general insurance distribution and nothing else. ‘The RICS Designated Professional Body scheme is a UK regulatory programme approved by HM Treasury, the UK’s ministry of finance. It enables us to regulate our members for general insurance distribution activities in the UK, on behalf of the Financial Conduct Authority.’[17]

RICS cannot, therefore, license its regulated firms or members to issue e-money or carry out payment services.

RICS Professional Standards

Countering financial crime: Bribery, corruption, money laundering, terrorist financing and sanctions violations[18]

RICS is, of course, aware of the regulations and every RICS-regulated firm and member is required to have an anti-money laundering policy. The current Professional Standard issued by RICS in July 2023 is unchanged from the Professional Statement previously published in February 2019.[19] An updated standard has been published in draft for consultation with RICS members, a process which ended in April 2025.

The 2019 and 2023 documents both confirm that:

RICS-regulated firms undertaking activity in the following areas must register with HMRC. There are some very limited exceptions which allow some businesses to not register for supervision.

However, even if a firm is exempt from formal money laundering supervision, this does not mean that it does not have to be concerned about money laundering risks. All firms have a responsibility under the Proceeds of Crime Act 2002 and RICS own professional standards and guidance.

The list of activity areas comprises estate agency, lettings agency, property management, accountancy and tax services, company services, and valuation and tax advice. None of these activities is covered by the Regulated Activities Order suggesting that RICS was not contemplating that members would be offering payment services outside these specific areas. Indeed, enter ‘escrow services’ in the search box on the RICS website and it will return ‘searching instead for escort services’. Happily, it could not find any direct reference to those either.

This list does not appear in the draft second edition, which simply states at paragraph 1.1 that ‘This professional standard applies globally to all RICS-regulated firms and members. In cases where this standard contradicts local legislation, the legislation takes precedence.’

The draft second edition makes no reference to specific UK local legislation or the requirement for registration or authorisation by FCA and HMRC. It does, however, set out RICS requirements in respect of anti-money laundering risks and procedures including risk assessment, KYC due diligence, source of funds, identification of beneficial owners, record keeping and policies. These requirements appear broadly in line with the requirements of PSR 2017 and AMLR 2017 as they apply to a PSP holding security for expenses.

Client money handling

Members and regulated companies offering services as managing agents, services under the PWA, or indeed anything else using RICS regulated client accounts are covered by the RICS Client Money Handling Professional Standard,[20] which defines ‘client money’ as:

Money of any currency (whether in the form of cash, cheque, draft or electronic transfer) that:

- an RICS-regulated firm holds for or receives on behalf of another person, including money held by a regulated firm as stakeholder and

- is not immediately due and payable on demand to the RICS-regulated firm for its own account, excluding fees paid in advance for professional work agreed to be performed, and clearly identifiable as such, unless the fees are for work undertaken as a property agent as defined by the Rules of the RICS Client Money Protection Scheme for Property Agents.

Clearly, this would include security for expenses under the PWA.

Paragraph 2.2.6 requires RICS-regulated firms to:

- ensure compliance with all anti-money laundering legislation, rules and regulations for all receipts of client money

- ensure compliance with the mandatory requirements of the latest edition of RICS’ Countering bribery and corruption, money laundering and terrorist financing

- …

Paragraph 2.3 extends these requirements to individual RICS members.

Paragraph 3.6 provides:

As part of the requirement to comply with anti-money laundering standards, firms should ensure that all client money held is linked to a surveying activity being undertaken by the firm and that their client money account is therefore not being used as a banking facility for third parties, whether they are clients or not.

It is logical to conclude that by including this proviso RICS intended prohibiting client accounts being used for banking facilities in the same way that rule 3.3 of the Solicitors Account Rules applies to companies regulated by the SRA, leading to its warning against improper use of client accounts issued in 2014.

CONCLUSION

This review of UK financial services legislation, official guidance on its application, and direct engagement by the author with both FCA and HMLR confirms that:

- The holding of security for expenses under the PWA is a payment service as defined in PSR 2017, falling under service (f) money remittance. Regulated activities under FSMA 2000 do not include Payment Services as defined in PSR 2017.

- The ‘occasional or very limited basis’ exclusion under AMLR 2017 regulation 15(2) is not available for money remittance.

- Escrow services comprising the transfer of funds from a payer to a payee require registration or authorisation by the FCA even if provided as part of a package with other services.

- Where holding security is intrinsically linked to another activity, such as appointment or selection under section 10 of the PWA, although the service may be regarded as ancillary to that primary activity, it is still Money Remittance and would not qualify for exclusion.

- Under AMLR 2017, anyone holding security for expenses under the PWA is a PSP and must be supervised for AMLR by a supervisory authority.

- RICS is not included in the list of designated supervisory authorities in AMLR 2017 Schedule 1.

- Anyone, including RICS-regulated firms and members holding security for expenses under the PWA must register with the FCA as a SPI or an API.

- Exempt Professional Firms licensed by RICS under FSMA 2000 must register with the FCA, but RICS can no longer license them to hold security under the PWA.

EPILOGUE

PSR 2017 regulation 138 warns:

(1) A person may not provide a payment service in the United Kingdom, or purport to do so, unless the person is—

(a) an authorised payment institution;

(b) a small payment institution;

(c) …

It will come as a shock and surprise to some that what seems on the face of it to be a simple and obvious service is subject to such stringent regulation. Compliance has been dismissed by some practitioners as excessive, over complicated and even irrelevant but, as RICS observes in the forthcoming update to its Practice Standard:[21]

As financial crimes continue to evolve, these updates are essential to ensure that RICS-regulated firms and members remain equipped to effectively address a broad range of risks. The updated standard explains to RICS-regulated firms and members how to detect, prevent, and respond to emerging financial crime threats, while ensuring compliance with international regulations.

Compliance is onerous, but failure to comply can have serious consequences including not merely reputational damage but ‘imprisonment for a term not exceeding two years …’.[22]

In its continuing work to reduce unregulated activity and guide consumers the FCA introduced its Firm Checker service in 2026. Members of the public and prudent surveyors mindful of their statutory, quasijudicial role,[23] should use this service to confirm the status of any firm offering to hold security.

It is now very easy to check if someone is registered with just a couple of clicks. Under the service category ‘Payments and e-money, for example, online wallets and money transfers’ it should confirm that the firm has permission to ‘Transfer money for you without you holding an account’.

The Firm Checker will also confirm ‘What this firm can’t do’ and some permissions do not allow firms to make payments without the consent of the person giving security, which rather defeats the object of security for expenses.

References and Notes

(1) The Warning Notice issued by the SRA on 18th December, 2014 is no longer available on the SRA website, but we do have a copy. It includes a comprehensive discussion on the implications of ‘Improper use of a client account as a banking facility’.

(2) In English law, escrow refers to the conditional delivery of a deed after execution; that is, where a deed only becomes binding once one or more conditions precedent is fulfilled.

(3) Financial Conduct Authority (FCA), ‘FCA Handbook Perimeter Guidance Manual (PERG)’, Ch. 15, p. 20, available at https://handbook.fca.org.uk/handbook?entityId=perg (accessed 11th November, 2025).

(4) Legislation, ‘The Electronic Money Regulations 2011 SI 2011 No 99’, Gov. UK, available at www.legislation.gov.uk/uksi/2011/99/data.pdf (accessed 11th November, 2025).

(5) Financial Conduct Authority (FCA), ‘FCA Handbook’, available at https://handbook.fca.org.uk/handbook (accessed 11th November, 2025).

(6) Financial Conduct Authority (FCA), ref. 3 above.

(7) Trivvy, ‘Guidance on the scope of the Payment Services Regulations 2017’, Ch. 15, available at https://www.trivvy.nl/uploads/5/1/6/0/51608851/guidance_on_the_scope_of_the_payment_services_regulation_2017__march_2018_.pdf (accessed 11th November, 2025).

(8) Financial Conduct Authority (FCA) (November 2024), ‘Payment Services and Electronic Money – Our Approach’, Version 6, available at https://www.fca.org.uk/publication/finalised-guidance/fca-approach-payment-services-electronic-money-2017.pdf (accessed 11th November, 2025).

(9) Financial Conduct Authority (FCA) (December 2025), ‘Pre-application support service (PASS)’, available at https:// www.fca.org.uk/firms/authorisation/pre-application-support-service (accessed 11th November, 2025).

(10) Financial Conduct Authority (FCA), ref. 3 above, Ch. 15, p. 15/5.

(11) Financial Conduct Authority (FCA) (March 2025), FCA Pre-Application Support Service, (case ref: 211494671).

(12) If the total payments in a 12-month period do not exceed an average of €3m per month, a provider can register with the FCA as a SPI.

(13) If the total payments in a 12-month period exceed the above limit, the provider must apply for authorisation, which is a more onerous regulatory regime.

(14) The appointment of a surveyor under the PWA can only be confirmed once a dispute has arisen or been deemed to arise which can only happen after a notice has been served. It is normal for a building owner to engage a surveyor to advise and serve the notice that then triggers the dispute.

(15) The provisions relating to sale and rent back agreements were clarified in The Financial Services and Markets Act 2000 (16) (17) (18) (19) (20) (Regulated Activities) (Amendment) Order 2009. Legislation, ref. 4 above, p. 66.

Royal Institution of Chartered Surveyors (RICS), ‘Designated Professional Body Scheme for General Insurance Distribution (UK)’, available at https://www.rics.org/regulation/regulatory-schemes/designated-professional-body-scheme (accessed 11th November, 2025).

Royal Institution of Chartered Surveyors (RICS) (February 2019), ‘Countering financial crime: Bribery, corruption, money laundering, terrorist financing and sanctions violations’, 1st edn, available at https://www.rics.org/content/dam/ricsglobal/documents/standards/February_2019_Countering_Bribery_And_Corruption_Money_Laundering_And_Terrorist_Financing_1st_Edition.pdf (accessed 11th November, 2025).

RICS Statements and Standards have different status. Royal Institution of Chartered Surveyors (RICS) (October 2019), ‘Client Money Handling’, 1st edn, available at https://www.rics.org/content/dam/ricsglobal/documents/regulation/client_money_handling_1st_edition.pdf (accessed 11th November, 2025).

(21) Royal Institution of Chartered Surveyors (RICS) (September 2025), ‘Countering financial crime: Bribery, corruption, money laundering, terrorist financing and sanctions violations’, 2nd edn, available at https://www.rics.org/content/dam/ricsglobal/documents/standards/Countering-financial-crime_2nd-edition_amended3.pdf (accessed 11th November, 2025).

(22) Legislation, ‘The Payments Services Regulations 2017’, Regulation 138(2)

(b), Gov.UK, available at https://www.legislation.gov.uk/uksi/2017/752/regulation/138#:~:text=Section%20138%20of%20the%20Payment%20Services%20Regulations,Ireland%20*%20Both%20imprisonment%20and%20a%20 fine (accessed 11th November, 2025).

(23) Brightman J, Gyle-Thompson v Wall Street (Properties) Ltd [1974] 1 WLR 123 p130H; Collins Rice J, R on the application of Subramanian v City of London Magistrates [2019] EWHC 1240 (Admin) at [52].